- What is Asset FinanceBack

What is Asset FinanceClose Brothers Asset Finance offer a range of flexible funding options enabling you to purchase assets and grow your business.Find out more

- Hire PurchaseSpread the cost over time

- RefinancingWhen you need a cash injection

- Finance LeaseUser benefits without the ties of ownership

- Operating LeaseKeep your options open

- Assets for saleBack

Assets for saleHere at Close Brothers Asset Finance, we have a wide variety of used vehicles for sale, including ex lease vehicles and equipment.See our assets for sale

- Find your industryBack

Find your industryClose Brothers Asset Finance supports various industries across the UK. Click on your industry to find out how we can support your business.Our industries

Agriculture is a crucial part of the UK economy and we have specialist knowledge of agricultural equipment finance and understand the challenges and opportunities facing both the agricultural and forestry industries

Our dedicated team of agricultural and forestry specialists have extensive knowledge and experience of both industries, which gives them the ability to confidently support you and your business.

They understand the challenges businesses in the agricultural sectors face, including the high running costs from equipment and machinery that can make it difficult to raise the necessary capital to support growth plans.

Our process is simple but effective – our agricultural team will work closely with you to create a finance agreement that works for you.

For example, that could be releasing capital from an existing asset to invest in new equipment or spreading the cost of your repayments to match your seasonal income.

Using our specialist knowledge, we will guide you through the application process, enabling you to take full advantage of the benefits of asset finance including Hire Purchase, Finance Lease, Operating Lease and Refinance packages.

Get in touch with our agricultural team today.

Typical agricultural and forestry assets we fund include:

- Tractor financing

- Combine harvesters

- Field sprayers

- Horseboxes

- Milking parlours (robotic and rotary)

- Forestry machinery (harvester, forwarder, skidder)

- Timber processing equipment

- Woodchippers

- Solar PV, biomass boilers, wind turbines

- Portacabins

- Modular buildings, welfare units, glamping pods

- Ground care equipment

- Other farming and agricultural equipment

Contact us today

9:00am - 5:00pm Monday to Friday (excluding UK bank holidays)

Finance products we offer the agricultural and forestry industries

What is Hire Purchase?

How Hire Purchase works

Hire Purchase is a great way to get what you need because you get to choose, use and manage the assets you need for your business over an agreed period, typically up to five years.

The regular instalments you pay as part of your agreement will cover:

- The asset's depreciation

- Interest on the cost of the asset

At the end of the term, you get to choose to buy the asset and own it outright.

Who is Hire Purchase for?

Hire Purchase is especially handy for:

- Businesses who want to keep control of their cash flow by knowing what their investments are going to cost them over the long-term, allowing them to budget effectively

- Purchasing ‘hard’ assets like vehicles, machinery, equipment and other assets with resale value

Advantages of Hire Purchase:

- More time to repay: By spreading the cost over the life of the asset, a benefit is that you can lower the initial up-front payment. This matters because it gives you a long-term view of the fixed monthly payments you will need to make over the term of the agreement, which – in turn- helps you with your budgeting

- Seasonality: If your business – like many others – has busy times and less busy times throughout the year, your monthly repayments can be adjusted in line with your sales peaks and troughs. For example, during the lead into the festive season your sales volumes might peak, but in the month or two after New Year, they fall back

- Keep control: With Hire Purchase, you're in charge. You get full use of the asset throughout the repayment period and may even claim capital allowance. Capital allowance is a type of tax relief that businesses can claim when they spend money on long-term assets for use in the business. You can deduct some or all of the value of the asset from your taxable profit

- Tax efficient: Financing your asset purchase through Hire Purchase can be tax-friendly because lease payments are treated as expenses, offering potential tax benefits compared to standard loans. Although asset depreciation also provides tax benefits, the useable lifetime of the asset will vary depending on the asset and on local regulation

- Reclaim VAT: If you're VAT registered, you may reclaim VAT. For details on VAT registration, visit gov.uk/vat-registration/overview

Finance is secured against the asset and/or equipment. If you're unable to keep up with your payments we may repossess the asset and/or equipment.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

What is Refinance?

How Refinance works

Refinancing uses the value of assets you already own to help your business. With Sale and HP Back – a type of refinancing – you sell your equipment to us, and we lend you the money you need to invest in your business.

You pay us back in line with what the equipment earns for you. Once you’re done paying us back, you own the equipment again.

This works whether you own the equipment outright or are already financing it with someone else.

Who is Refinancing for?

Refinancing is for anyone looking to unlock the value of their existing assets to support their business. Whether you own equipment outright or are financing it elsewhere, refinancing can provide a quick way to access funds for things like new equipment, improving cash flow, or other business needs.

It’s a flexible option suitable for businesses of all sizes, including sole traders.

Advantages of Refinance:

- Get more cash easily: Asset refinancing is a quick and simple way to get extra money for your business needs. You get to keep using the asset you put up as security.

- Pay over a longer time: We can take over your current financing deal with another company and extend the time you have to pay. The costs are fixed, so there won't be any surprises while you're repaying the loan.

- Choose what's best for you: Use the cash injection for your business or buy other things you need. It's more flexible than some other financing options.

- Decide quickly: Getting cash from your assets helps you make faster decisions when dealing with business contracts. Use the money for hiring people, buying new things, or expanding your workspace.

Finance is secured against the asset and/or equipment. If you're unable to keep up with your payments we may repossess the asset and/or equipment.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

What is Finance Lease?

How Finance Lease works

Think of Finance Lease as a long-term rental for business assets (or equipment, which is the same thing). Instead of buying the asset upfront, you pay rent to use it, with a flexible rental period to match your needs and cash flow fluctuations, which we know can change month-to-month. You cover the cost of the payments, including the agreed interest, for the duration of the rental period.

At the end of the initial lease, you have various options available to you:

- Keep on using: Continue leasing the asset by extending the rental period – otherwise known as a ‘secondary rental period’

- Sell and earn: You can sell the equipment and keep a share of what the asset is sold for

- Return: Give the equipment back to us if you no longer need it or want to upgrade to something newer

Who is Finance Lease for?

Finance lease is for businesses that need equipment but prefer not to purchase it outright. It's suitable for companies looking to use assets like machinery, vehicles, or technology without a large upfront cost. Whether you're a small construction firm needing a forklift or a larger operation needing specialist equipment, finance lease offers flexibility by allowing you to pay for the equipment over time while having the option to keep, sell, or return it at the end of the lease term.

Advantages of Finance Lease:

- Get what you need without a big upfront cost: You can quickly get the equipment you want without paying a large sum upfront. Instead, payments are broken into monthly instalments.

- Customise payments to match your cash flow: Work with us to adjust the rental payments and lease periods to match how and when money comes into your business.

- Earn money back: If you decide to sell the equipment at the end of the lease, you will get money from the sale.

- Tax Benefits: If your business is VAT registered, you only pay VAT on the monthly rental payments, not on the entire purchase price. This helps reduce your taxable profit, potentially saving you money on taxes. If your business is not VAT registered, you can spread the VAT cost by including it in your monthly rental rather than paying it as a one-off payment.

- For more information on VAT registration, please visit gov.uk/vat-registration/overview

Finance is secured against the asset and/or equipment. If you're unable to keep up with your payments we may repossess the asset and/or equipment.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

What is Operating Lease?

How Operating Lease works

In common with Finance Lease, an Operating Lease lets you rent the asset from us for the duration you require it.

The main difference lies in the fact that an Operating Lease covers only a portion of the asset's total useful life meaning you pay a lower rental fee because it's calculated based on the difference between the asset's initial purchase cost and its residual value at the agreement's end.

You enjoy complete access to the asset for your required duration, without the obligation of managing its disposal or recovering its residual value.

Who is Operating Lease for?

Operating Lease is suitable for businesses that need equipment but prefer not to purchase it outright. It means you can use equipment, vehicles, or technology without a large upfront cost while paying a lower monthly rental fee.

Advantages of Operating Lease:

- Affordable start: Get the asset you need without a big upfront cost

- Complete usage freedom: Use the asset fully without buying it outright

- Flexible choices: Decide at the end of the term whether to re-rent, buy, or return the asset

- Lower payments: Rental cost is less because it's a percentage of the initial cost

- Cost savings: Reclaim VAT on rentals to reduce overall costs

Finance is secured against the asset and/or equipment. If you're unable to keep up with your payments we may repossess the asset and/or equipment.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Hire Purchase What is Hire Purchase?

How Hire Purchase works

Hire Purchase is a great way to get what you need because you get to choose, use and manage the assets you need for your business over an agreed period, typically up to five years.

The regular instalments you pay as part of your agreement will cover:

- The asset's depreciation

- Interest on the cost of the asset

At the end of the term, you get to choose to buy the asset and own it outright.

Who is Hire Purchase for?

Hire Purchase is especially handy for:

- Businesses who want to keep control of their cash flow by knowing what their investments are going to cost them over the long-term, allowing them to budget effectively

- Purchasing ‘hard’ assets like vehicles, machinery, equipment and other assets with resale value

Advantages of Hire Purchase:

- More time to repay: By spreading the cost over the life of the asset, a benefit is that you can lower the initial up-front payment. This matters because it gives you a long-term view of the fixed monthly payments you will need to make over the term of the agreement, which – in turn- helps you with your budgeting

- Seasonality: If your business – like many others – has busy times and less busy times throughout the year, your monthly repayments can be adjusted in line with your sales peaks and troughs. For example, during the lead into the festive season your sales volumes might peak, but in the month or two after New Year, they fall back

- Keep control: With Hire Purchase, you're in charge. You get full use of the asset throughout the repayment period and may even claim capital allowance. Capital allowance is a type of tax relief that businesses can claim when they spend money on long-term assets for use in the business. You can deduct some or all of the value of the asset from your taxable profit

- Tax efficient: Financing your asset purchase through Hire Purchase can be tax-friendly because lease payments are treated as expenses, offering potential tax benefits compared to standard loans. Although asset depreciation also provides tax benefits, the useable lifetime of the asset will vary depending on the asset and on local regulation

- Reclaim VAT: If you're VAT registered, you may reclaim VAT. For details on VAT registration, visit gov.uk/vat-registration/overview

Finance is secured against the asset and/or equipment. If you're unable to keep up with your payments we may repossess the asset and/or equipment.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Refinance / Capital Release What is Refinance?

How Refinance works

Refinancing uses the value of assets you already own to help your business. With Sale and HP Back – a type of refinancing – you sell your equipment to us, and we lend you the money you need to invest in your business.

You pay us back in line with what the equipment earns for you. Once you’re done paying us back, you own the equipment again.

This works whether you own the equipment outright or are already financing it with someone else.

Who is Refinancing for?

Refinancing is for anyone looking to unlock the value of their existing assets to support their business. Whether you own equipment outright or are financing it elsewhere, refinancing can provide a quick way to access funds for things like new equipment, improving cash flow, or other business needs.

It’s a flexible option suitable for businesses of all sizes, including sole traders.

Advantages of Refinance:

- Get more cash easily: Asset refinancing is a quick and simple way to get extra money for your business needs. You get to keep using the asset you put up as security.

- Pay over a longer time: We can take over your current financing deal with another company and extend the time you have to pay. The costs are fixed, so there won't be any surprises while you're repaying the loan.

- Choose what's best for you: Use the cash injection for your business or buy other things you need. It's more flexible than some other financing options.

- Decide quickly: Getting cash from your assets helps you make faster decisions when dealing with business contracts. Use the money for hiring people, buying new things, or expanding your workspace.

Finance is secured against the asset and/or equipment. If you're unable to keep up with your payments we may repossess the asset and/or equipment.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Finance Lease What is Finance Lease?

How Finance Lease works

Think of Finance Lease as a long-term rental for business assets (or equipment, which is the same thing). Instead of buying the asset upfront, you pay rent to use it, with a flexible rental period to match your needs and cash flow fluctuations, which we know can change month-to-month. You cover the cost of the payments, including the agreed interest, for the duration of the rental period.

At the end of the initial lease, you have various options available to you:

- Keep on using: Continue leasing the asset by extending the rental period – otherwise known as a ‘secondary rental period’

- Sell and earn: You can sell the equipment and keep a share of what the asset is sold for

- Return: Give the equipment back to us if you no longer need it or want to upgrade to something newer

Who is Finance Lease for?

Finance lease is for businesses that need equipment but prefer not to purchase it outright. It's suitable for companies looking to use assets like machinery, vehicles, or technology without a large upfront cost. Whether you're a small construction firm needing a forklift or a larger operation needing specialist equipment, finance lease offers flexibility by allowing you to pay for the equipment over time while having the option to keep, sell, or return it at the end of the lease term.

Advantages of Finance Lease:

- Get what you need without a big upfront cost: You can quickly get the equipment you want without paying a large sum upfront. Instead, payments are broken into monthly instalments.

- Customise payments to match your cash flow: Work with us to adjust the rental payments and lease periods to match how and when money comes into your business.

- Earn money back: If you decide to sell the equipment at the end of the lease, you will get money from the sale.

- Tax Benefits: If your business is VAT registered, you only pay VAT on the monthly rental payments, not on the entire purchase price. This helps reduce your taxable profit, potentially saving you money on taxes. If your business is not VAT registered, you can spread the VAT cost by including it in your monthly rental rather than paying it as a one-off payment.

- For more information on VAT registration, please visit gov.uk/vat-registration/overview

Finance is secured against the asset and/or equipment. If you're unable to keep up with your payments we may repossess the asset and/or equipment.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Operating Lease What is Operating Lease?

How Operating Lease works

In common with Finance Lease, an Operating Lease lets you rent the asset from us for the duration you require it.

The main difference lies in the fact that an Operating Lease covers only a portion of the asset's total useful life meaning you pay a lower rental fee because it's calculated based on the difference between the asset's initial purchase cost and its residual value at the agreement's end.

You enjoy complete access to the asset for your required duration, without the obligation of managing its disposal or recovering its residual value.

Who is Operating Lease for?

Operating Lease is suitable for businesses that need equipment but prefer not to purchase it outright. It means you can use equipment, vehicles, or technology without a large upfront cost while paying a lower monthly rental fee.

Advantages of Operating Lease:

- Affordable start: Get the asset you need without a big upfront cost

- Complete usage freedom: Use the asset fully without buying it outright

- Flexible choices: Decide at the end of the term whether to re-rent, buy, or return the asset

- Lower payments: Rental cost is less because it's a percentage of the initial cost

- Cost savings: Reclaim VAT on rentals to reduce overall costs

Finance is secured against the asset and/or equipment. If you're unable to keep up with your payments we may repossess the asset and/or equipment.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Get the additional funds you need

A chattel mortgage is, very simply, a loan arrangement where movable assets (‘chattels’) – like vehicles, machinery, and equipment – are used as security for a loan.

Chattel mortgages are commonly used for financing assets like commercial vehicles, manufacturing equipment, or office machinery, and are a way for businesses to secure loans using their movable assets as collateral, making it an alternative to traditional mortgages.

How it works:

- The borrower enters into an agreement with Close Brothers Asset Finance, where the borrower agrees to repay the loan, while we as the lender take a security interest in a specified chattel.

- Close Brothers Asset Finance’s interest in the chattel serves as security for the loan. If the borrower defaults on the loan, we as the lender have the right to take possession of and potentially sell the chattel to recover the outstanding debt.

- The borrower still owns the chattel during the loan period, but Close Brothers Asset Finance has a legal claim over it until the loan is paid off.

- The borrower makes regular payments to repay the loan, and once the loan is fully repaid, Close Brothers Asset Finance releases its interest in the chattel, and ownership is fully transferred back to the borrower.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Make payments in line with your cashflow

Seasonal Repayments are loans that are structured in a way that match your business’s income and cashflow, and are particularly useful for sectors with seasonal trading periods, including agriculture, tourism and hospitality.

Agreements are customised and tailored to meet your specific demands, meaning you make larger repayments when your income is strong and smaller repayments during quieter times.

Your options:

- Low start payments can alleviate the challenge of having to pay for an asset before it begins paying for itself without the need to raise additional working capital.

- Seasonal low repayments are for firms that have trading fluctuations at different times of the year and is a way to reduce the effect of annual trading lows without needing to borrow more.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Delay paying the VAT on your new asset

When you use Hire Purchase to fund a piece of equipment or machinery, you will typically pay for the asset in monthly, quarterly or annual instalments over a set period of time.

VAT usually needs to be paid upfront and while it can be reclaimed later, it can have a big impact on cashflow.

How it works:

To overcome this, we offer a VAT deferral to give you a longer time to pay and time to reclaim the VAT on the asset you purchased. You can delay your VAT payment for up to four months from the date of the finance agreement.

VAT is taken automatically by Direct Debit at months 1, 2, 3 or 4 depending on when you decide is best for your cash flow.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Chattel Mortgage Get the additional funds you need A chattel mortgage is, very simply, a loan arrangement where movable assets (‘chattels’) – like vehicles, machinery, and equipment – are used as security for a loan.

Chattel mortgages are commonly used for financing assets like commercial vehicles, manufacturing equipment, or office machinery, and are a way for businesses to secure loans using their movable assets as collateral, making it an alternative to traditional mortgages.

How it works: - The borrower enters into an agreement with Close Brothers Asset Finance, where the borrower agrees to repay the loan, while we as the lender take a security interest in a specified chattel.

- Close Brothers Asset Finance’s interest in the chattel serves as security for the loan. If the borrower defaults on the loan, we as the lender have the right to take possession of and potentially sell the chattel to recover the outstanding debt.

- The borrower still owns the chattel during the loan period, but Close Brothers Asset Finance has a legal claim over it until the loan is paid off.

- The borrower makes regular payments to repay the loan, and once the loan is fully repaid, Close Brothers Asset Finance releases its interest in the chattel, and ownership is fully transferred back to the borrower.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Seasonal Repayments Make payments in line with your cashflow Seasonal Repayments are loans that are structured in a way that match your business’s income and cashflow, and are particularly useful for sectors with seasonal trading periods, including agriculture, tourism and hospitality.

Agreements are customised and tailored to meet your specific demands, meaning you make larger repayments when your income is strong and smaller repayments during quieter times.

Your options: - Low start payments can alleviate the challenge of having to pay for an asset before it begins paying for itself without the need to raise additional working capital.

- Seasonal low repayments are for firms that have trading fluctuations at different times of the year and is a way to reduce the effect of annual trading lows without needing to borrow more.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

VAT defferals Delay paying the VAT on your new asset When you use Hire Purchase to fund a piece of equipment or machinery, you will typically pay for the asset in monthly, quarterly or annual instalments over a set period of time.

VAT usually needs to be paid upfront and while it can be reclaimed later, it can have a big impact on cashflow.

How it works: To overcome this, we offer a VAT deferral to give you a longer time to pay and time to reclaim the VAT on the asset you purchased. You can delay your VAT payment for up to four months from the date of the finance agreement.

VAT is taken automatically by Direct Debit at months 1, 2, 3 or 4 depending on when you decide is best for your cash flow.

Products and services are subject to eligibility, status, terms and conditions and availability. All lending is subject to status and our lending criteria. The right to decline any application is reserved.

Agriculture news and insights

Supporting a three-generation family farm

CASE STUDIES10 Mar 2026

Supporting a young entrepreneur in Agricultural contracting

CASE STUDIES11 Jun 2025

Diversification opportunities for farmers

BLOG01 Apr 2025

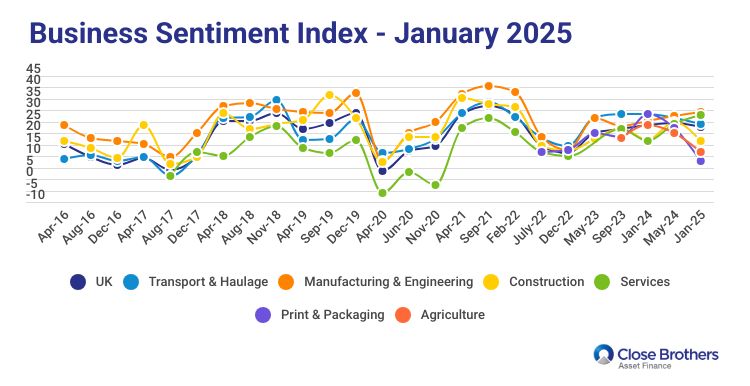

Confidence dips among UK SMEs, but positivity in key sectors improves

BUSINESS BAROMETER06 Feb 2025

Tree surgery business uses Finance Lease to access essential equipment

CASE STUDIES29 Aug 2024

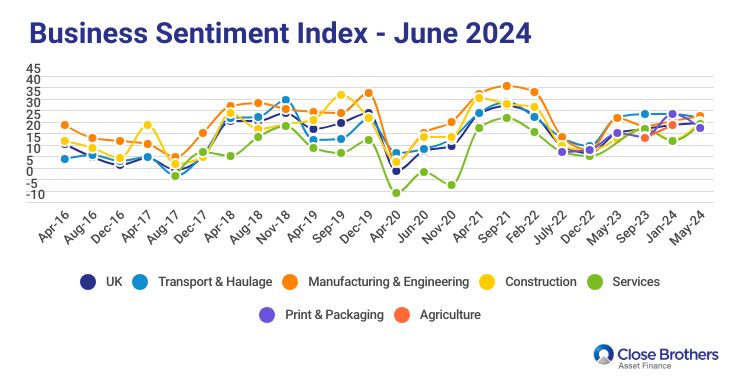

Business Sentiment Index – confidence among SMEs continues to edge up

BUSINESS BAROMETER17 Jun 2024